IVF Insurance Coverage in NY and NJ

New York and New Jersey are mandated states, which means state law requires many insurance providers to cover IVF. Patients in both states have enforceable access to coverage that most of the country lacks.

But ‘mandated’ doesn’t mean universal. Since coverage varies by policy, you’ll want to verify your benefits early to avoid unexpected out-of-pocket costs.

Here’s what you need to know before you start IVF in New York or New Jersey.

New York’s IVF Mandate

New York has a long history of protecting fertility access. Enacted in 2002, the state’s insurance law was modernized in 2019 and further strengthened in 2024.

Under the current law, all fully insured commercial plans in New York—including individual, small group, and large group markets—must cover basic infertility care when a patient meets the clinical definition of infertility.

- Under age 35: The failure to establish a clinical pregnancy after 12 months of regular, unprotected sexual intercourse or therapeutic donor insemination.

- Age 35 and older: Failure to establish a clinical pregnancy after 6 months of regular, unprotected sexual intercourse or therapeutic donor insemination.

Coverage for infertility care includes diagnosis, diagnostic testing, and treatments such as intrauterine insemination (IUI).

When it comes to IVF coverage, large group plans, including employers with more than 100 employees, must cover up to three IVF cycles per lifetime. One cycle means one complete attempt, from ovarian stimulation and egg retrieval through either a fresh or frozen embryo transfer. This includes medications and embryo storage connected to a covered cycle. Patients must be between 21 and 44.

The law also prohibits discrimination based on age, sex, sexual orientation, marital status, or gender identity. Insurers can’t deny coverage for single patients and same-sex couples based on their relationship status.

For patients with cancer or other diagnoses facing treatments that may cause infertility, all New York commercial markets, including individual and small group plans, must cover medically necessary fertility preservation. This accounts for egg freezing and sperm banking ahead of chemotherapy, radiation, or surgery.

While there’s no defined storage time limit under state law, plans may apply medical necessity review.

New Jersey’s IVF Mandate

New Jersey’s infertility mandate, formally codified as the New Jersey Family Building Act, is one of the broader state-level policies in the country. For employers with 50 or more employees who provide pregnancy-related benefits and have fully insured plans in New Jersey, the law requires coverage for the diagnosis and treatment of infertility, including IVF.

Where New York caps coverage at three IVF cycles, New Jersey mandates coverage for up to four completed egg retrievals per lifetime. Insurers must cover each retrieval and the resulting embryo transfers. The law covers IVF using donor eggs and IVF where the embryo is transferred to a gestational carrier or surrogate, making New Jersey’s mandate among the most inclusive in the country to date. Injectable fertility medications are covered, even if the policy doesn’t otherwise include a prescription drug benefit.

Patients must be under 46 to qualify. Procedures must also be performed at a facility meeting standards set by the American Society for Reproductive Medicine (ASRM) or the American College of Obstetricians and Gynecologists (ACOG). Many plans require patients to have attempted less intensive treatments before approving IVF.

Like New York, New Jersey prohibits carriers from denying or delaying treatment based on age, sexual orientation, or relationship status. A 2024 update to the law expanded anti-discrimination protections and extended coverage to genetic testing and embryo transfers as discrete mandated services.

The Caveat That Catches Many Patients Off Guard

Both mandates share an important distinction: they apply only to fully insured plans.

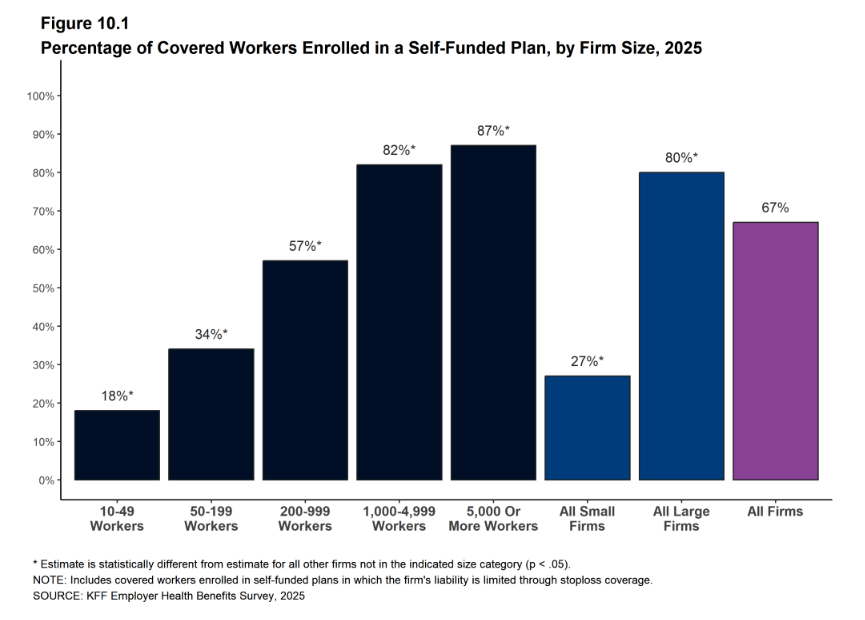

According to KFF’s 2025 Employer Health Benefits Survey, approximately 67% of Americans with employer-sponsored insurance are enrolled in self-insured or self-funded plans. Under federal ERISA law, self-insured employers are exempt from state insurance mandates, including those in New York and New Jersey.

With a fully insured plan, your employer pays premiums to an insurance company, which then assumes the financial risk of your claims. Employers must comply with state coverage mandates. With a self-insured plan, your employer funds claims directly, using an insurer for administration. This is why federal law, not state law, governs what it has to cover.

An employer headquartered in New Jersey with 500 employees can legally provide zero IVF coverage if their health plan is self-funded. Government programs, including Medicaid, are also generally not subject to IVF coverage requirements in either state.

Before starting treatment, ask your HR department whether your health plan is fully insured or self-insured. The answer to this question determines whether your state’s mandate applies to you.

What’s on the Docket for 2026

The New York State Senate advanced a legislative package in early 2026 that, if enacted, would expand IVF coverage for New Yorkers. The proposals include requiring coverage for donor egg retrievals and unlimited embryo transfers, prohibiting insurers from requiring women 35 and older to transfer all embryos from a prior cycle before approving a new one, and codifying IVF coverage protections for same-sex couples that currently exist as regulatory guidance rather than statute.

None of these provisions are law yet—they’re still in the legislature. New York is working to close the gaps in its existing mandate, particularly for patients who have historically faced coverage barriers around donor cycles. And while state mandates cover millions of patients, roughly two-thirds of Americans with employer-sponsored insurance are in self-funded plans that no state law can touch.

Americans for IVF is pushing to close that gap federally through the HOPE Act, which would require coverage for IVF regardless of plan type. Dr. Joshua Klein and Dr. Nataki Douglas, both of Extend Fertility, serve on the organization’s Advisory Board.

How to Confirm What Your Insurance Plan Covers

The first two questions you should ask: Is my plan fully insured, and what state is it regulated in?

If you’re a New York or New Jersey employee with a fully insured plan in the relevant state, the mandate likely applies. If you’re in a self-funded plan, the state mandate doesn’t apply. But many large employers have voluntarily adopted IVF benefits, so your plan documents may still include coverage.

From there, clarify the details:

- How many egg retrievals or cycles does your plan cover?

- What does a ‘cycle’ include?

- Are medications covered separately or as part of the cycle benefit?

- Does your plan require step therapy? In other words, do you have to try IUI first before your insurer will approve coverage for IVF?

At Extend Fertility, financial coordinators verify your coverage before treatment begins, walking you through what your specific plan covers. We’ll also let you know what prior authorization may be required and what out-of-pocket costs to expect.

Insurance is complicated, but it’s usually not the only path to treatment. Many clinics, including Extend, offer financing to ease the financial burden of fertility treatment. Our goal is for you to walk into your first appointment with clarity around your costs and coverage.

Schedule a consultation today to discuss your options.

Share